By Dan Cwalinski, Director of Contracts and Pricing

Following a two-year delay, PJM Interconnection held the 2022/2023 Base Residual Auction (BRA) from May 19, 2021 through May 25, 2021 and published the results on June 2, 2021. The 2022/2023 BRA is the third auction where PJM has procured 100% Capacity Performance Resources, which, according to PJM, are resources capable of sustained, predictable operation, and are expected to be available and capable of providing energy and reserves when needed throughout the entire Delivery Year.

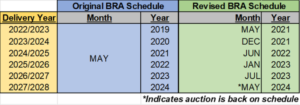

BRAs are typically held three years in advance of the Delivery Year, however, the 2022/2023 BRA that was originally scheduled for May 2019 was postponed while FERC considered changes to capacity market rules, principally the new Minimum Offer Price Rules (MOPR). This was the first BRA that concluded under the new MOPR, which requires PJM to establish resource based MOPRs for both new and existing resources that either collect, or are eligible to collect, state subsidies in order to prevent artificially low capacity prices.

PJM has since compressed the future BRA schedule to eventually return to a dynamic where the capacity auction is held three years in advance of the Delivery Year. The traditional BRA timing will resume in May 2024 with the 2027/2028 Delivery Year.

The 2022/2023 BRA concluded with the procurement of 144,477.3 MW of unforced capacity representing a reserve margin of about 19.9%. Resource

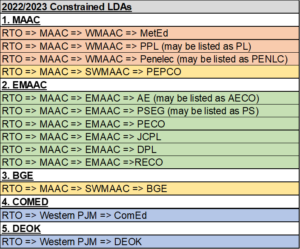

Clearing Prices (RCP) for the RTO in BRA 2022/2023 were $50/MW-day which is much lower than in BRA 2021/2022 where the RTO RCP was $140/MW-day. Constrained Locational Deliverability Areas (LDAs) for 2022/2023 were MAAC, EMAAC, BGE, COMED, and DEOK while constrained LDAs for 2021/2022 were EMAAC, PSEG, BGE, ATSI, and COMED.

A few elements that contributed to the lower 2022/2023 BRA resource clearing prices relative to 2021/2022 BRA are below:

Supply Side Elements:

Overall, offer prices from supply resources in BRA 2022/2023 were lower in this auction than the previous auction.

Demand Side Elements:

The forecasted peak load for the PJM RTO was lower for the 2022/2023 Delivery Year than for

the 2021/2022 Delivery Year by 2,418.4 MW or 1.6%. The lower forecasted peak load along with a lower Reserve Margin (19.9% versus 21.5%) and pool-wide Equivalent Demand Forced Outage Rate (EFORd) translated to a 3,086 MW decrease in the overall reliability requirement for the RTO compared to the 2021/2022 BRA.

The Net CONE (Cost of New Entry) also decreased by 19% for the RTO as well as each of the modeled LDAs. The decrease in the individual LDA Net CONE values varied from 7.4% in BGE to 28.0% for the COMED.

About Freedom Energy Logistics: Founded in 2006, Freedom Energy Logistics is a leading energy advisory. The private company offers comprehensive energy supply management and renewable energy solutions supporting energy goals and sustainability objectives for businesses and organizations throughout the U.S. Freedom’s team of energy experts has worked with and delivered energy saving, environmentally responsible solutions for some of the largest commercial and industrial companies, municipalities, universities, healthcare facilities, and businesses. With its headquarters located in Auburn, NH, Freedom Energy also has employees serving clients locally throughout the regions. Freedom Energy has been twice named to the Inc. 5000 list of fastest growing companies in America; recognized as one of the Fastest-Growing Family Businesses in NH by Business New Hampshire Magazine. Stay Work Play’s Coolest Company for Young Professionals; and received multiple Business Excellence Awards from New Hampshire Business Review. For more information, visit www.felpower.com.

Connect With Us